crude weekly insights – Fuel oil markets movements – Expected Major price fall in FO in India

Crude flat prices at pre-war levels. Pick up in SoH traffic, Production in the region coming back online, Asia’s tepid demand are the fundamental factors. Technically, Ongoing paper market selling continued to trigger oil price fall this week.

Timespreads dived with glut. Brent and Dubai benchmarks prompt price structure flipped into deep contango while WTI managed with narrow backwardation. Term structure refers to the relationship between the spot price and future contracts with different expiration dates. Term structure is always considered as the reliable market indicator signalling that oil markets are oversupplied.

Inventories data painted a bearish picture this week. A large draw in U.S crude (commercial and SPR) stocks reported while distillates and gasoline stocks were built up. Product stockpiles flooded into both Fujairah and SG markets w/w.

Refined product markets demonstrated bullish momentum as US gasoline cracks set a fresh all time seasonal high. The elevated pace of Ukraine attacks on Russia energy infra pushed the country to stop diesel exports and consider importing amid widening fuel shortage. U.S Diesel margins jumped $10/bbl on Russia’s supply shortage fears.

Market Positioning data showed that the speculators went shorter this past week. Money managers reduced their net length in Brent F&O triggered by capitulation. Both longs and shorts left the market.

FUEL OIL MARKETS

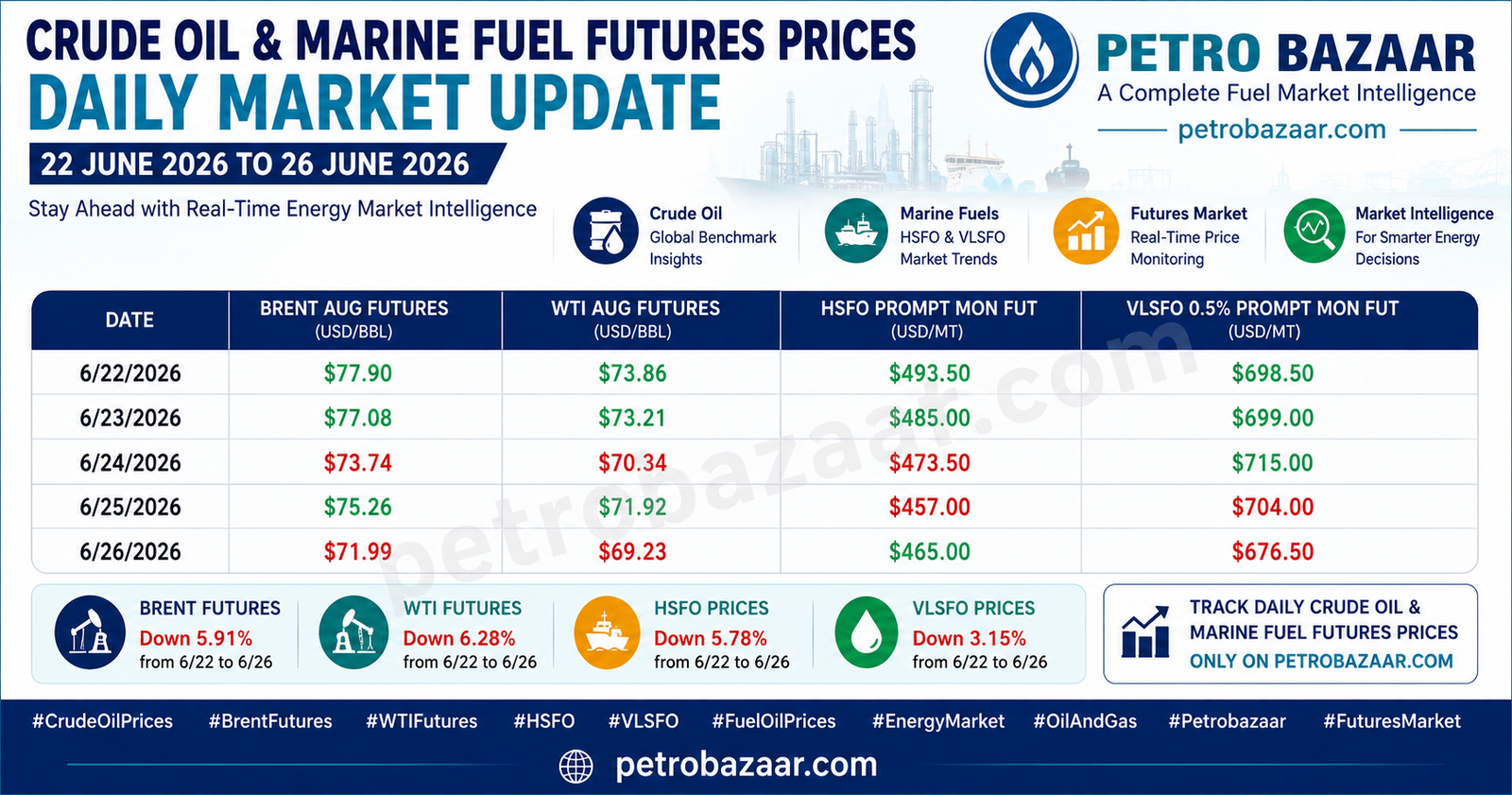

Singapore fuel oil markets ended the week on a weaker note, with HSFO flat prices declining by 5.8% from US$493.50/MT to US$465.00/MT, reflecting softer crude prices, weaker refinery demand, and improved regional supply. VLSFO prices remained comparatively resilient, easing 3.2% to US$676.50/MT after briefly strengthening mid-week on firmer marine fuel demand. Time spreads narrowed during the week, with both HSFO and VLSFO prompt spreads losing backwardation, indicating easing prompt supply tightness and a more balanced near-term market structure. The softer time spreads suggest reduced buying urgency from bunker suppliers and traders. Inventories at Singapore remained comfortable to slightly higher, supported by healthy arbitrage inflows from the Middle East and Western markets. Adequate stock availability continued to cap upside momentum despite intermittent bunker demand.

SENTIMENTAL ANALYSIS

Bearish to Neutral. Market participants remained cautious as falling crude oil prices, improving fuel oil availability, and subdued industrial demand outweighed support from seasonal bunker consumption.

PREDICTIVE ANALYTICS

VLSFO: Expected to remain stable with a mild downside bias around US$670–690/MT, supported by steady marine bunker demand but limited by comfortable inventories.

HSFO: Likely to trade range-bound to slightly bearish within US$455–475/MT, unless refinery outages or geopolitical disruptions tighten supply.

FO LDO PRICES ARE EXPECTED TO GO DOWN IN INDIA