crude weekly insights – Fuel oil markets movements – Expected Major price fall in FO in India

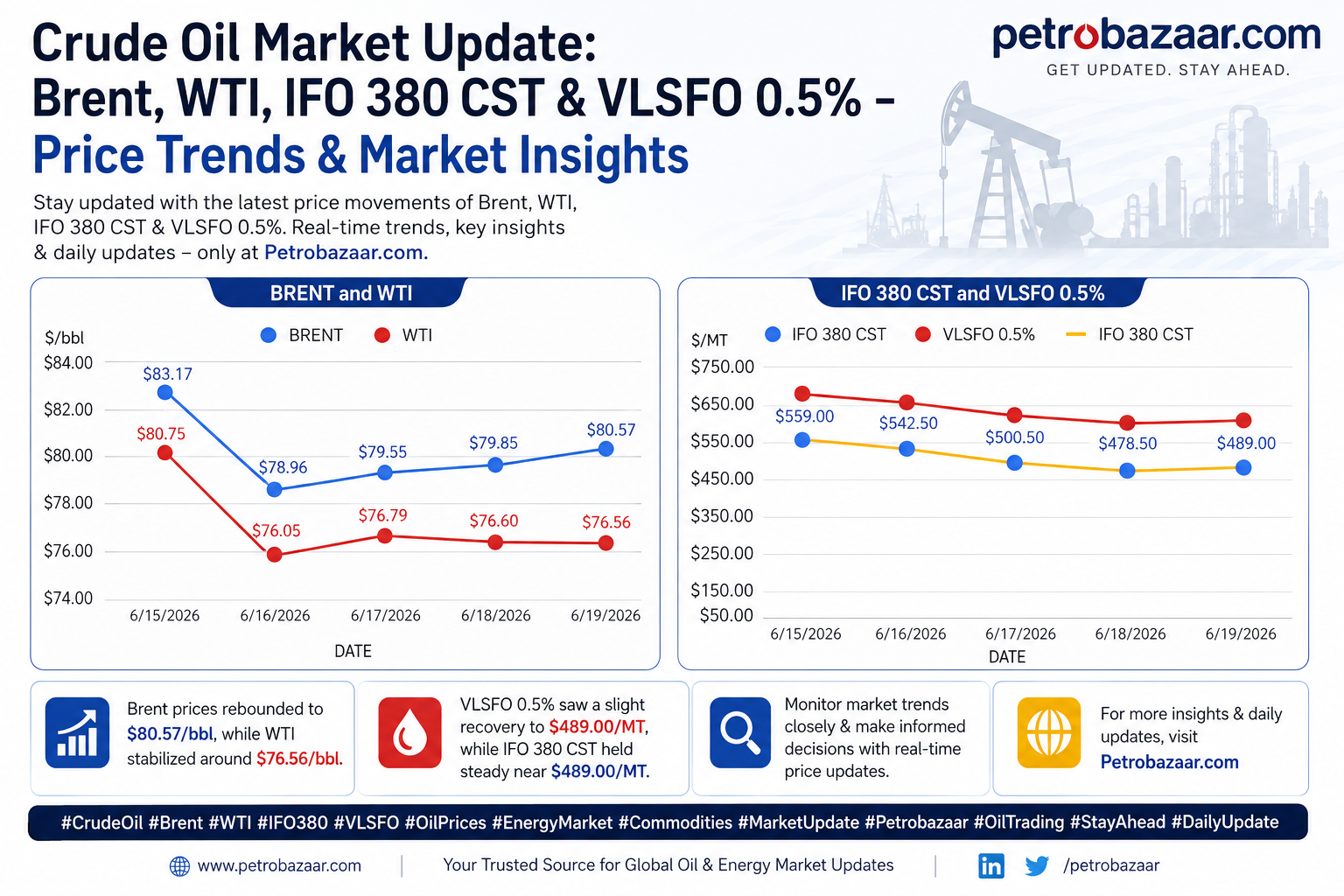

crude flat prices rose on Friday, Logged in weekly loss. U.S – Iran peace deal followed by optimism over free flow of supplies through SoH triggered bearish sentiment across. Trader’s agressive short selling also compounded the prevailing bearish mood. Markets were pricing in a deal and pretty seamless execution which we are not seeing so far.

Timespreads fell on the same fundamentals along with crude benchmarks. Both benchmarks on the edge of deep contango market structure. Contango is the market structure where future prices are higher than spot prices. Supply optimism keep weigh on oil fundamentals.

Inventories data showed that ARA Europe and US inventories continued to Crater across. Modest build reported in SG. product markets remains strong, Backed by gasoline tightness. US gasoline crack spreads demonstrated upside momentum.

Speculators were the net sellers of major petroleum F&O. Market Positioning data showed largest weekly reduction in Brent positions. Money managers reduced their net length in Brent crude oil F&O by 94763 to 114,128 in the week ending June 16th. Long only posiitons fell by 20,182 while short only positions rose by 74,581. Other reportables netlength rose by 22,903.

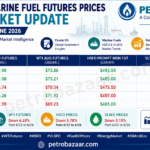

FUEL OIL MARKETS

Fuel oil markets demonstrated downside momentum during the week after a sharp fall in brent flat prices. HSFO remains under pressure compared to VLSFO. The VLSFO-HSFO spread widened. Ample supplies and sub-dued demand from Asia weighed on SG fuel oil markets. Front month fuel oil spreads softened on narrowing backwardation market structure shifting into contango structure due to change in supply fundamentals followed by peace deal. HSFO is likely to trade sideways with a mild upward bias if crude remains above $80/bbl while VLSFO should remain comparatively stronger due to bunker demand support. Fuel oil markets sentiment remains to be neutral. Furnace oil and Light diesel oil markets are moving for big price correction for the first half of July, 2026.