Petrobazaar.com Analysis & Insights

The International Energy Agency’s (IEA) Oil Market Report for November 2025 presents a mixed outlook for the global oil sector, marked by improving demand, strong supply growth, rising inventories, and softening crude prices. The market continues to navigate a delicate balance between economic recovery, geopolitical pressures, refining disruptions, and sanction-driven flows.

Global Demand: A Gradual Recovery Phase

Global oil demand witnessed a notable improvement in Q3 2025, expanding by nearly 920 kb/d year-on-year—more than double the growth recorded in Q2. Strong deliveries in China and a broadly improving macroeconomic environment underpinned this recovery.

The IEA maintains its full-year 2025 demand growth projection at ~790 kb/d, with demand expected to grow by ~770 kb/d in 2026. Although the recovery is strengthening, demand growth remains moderate by historical standards, underscoring a structurally cautious environment.

Global Supply: Strong Momentum Persists

Global oil supply reached 108.2 mb/d in October, despite recording a temporary decline of around 440 kb/d due to OPEC+ cuts and maintenance-related outages. Year-to-date, supply has surged by 6.2 mb/d, shared almost equally between OPEC+ and non-OPEC producers.

For 2025 and 2026, the IEA forecasts robust supply growth of 3.1 mb/d and 2.5 mb/d respectively. This continued build-up in supply, unless met with stronger consumption, sets the stage for a potential oversupplied market in the coming quarters.

Refining & Inventories: Tight Margins Amid Rising Stocks

Global refinery runs fell by 2.9 mb/d in October to 81.5 mb/d, owing to seasonal maintenance and unexpected outages. This tightening of product supply pushed middle-distillate margins in Europe and Asia to two-year highs.

However, the drop in refining activity contributed to rising stock levels:

- Observed global crude inventories climbed by 77.7 million barrels in September, the highest since 2021.

- Oil on water surged by nearly 80 million barrels, with Russian sanctioned barrels continuing to amplify floating stocks.

The build-up of inventories—both onshore and offshore—signals that supply is consistently outpacing refining throughput and consumption.

Crude Prices: Softening Under Supply Pressure

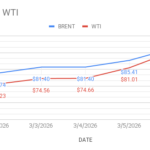

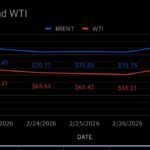

The North Sea benchmark Dated Brent averaged $64.64/bbl in October, down $3.26 from September. By mid-November, prices were tracking near $62/bbl amid rising stocks and strong supply flows.

While crude prices weakened, refiners benefitted from elevated margins, particularly for diesel and kerosene, due to constrained product availability and planned maintenance.

Market Balance & Risks: A Delicate Outlook

The IEA describes the market as “increasingly askew”, with strong supply growth overshadowing modest demand gains. Key uncertainties include:

- Geopolitical tensions and evolving sanctions impacting Russian flows

- Potential refining disruptions heading into winter

- Macroeconomic volatility across major consuming economies

- Trade and inflation-related risks that could affect fuel consumption

Given these factors, the oil market remains vulnerable to sudden shifts, with either unexpected supply cuts or economic weakness capable of altering the balance quickly.

Implications for the Indian Market

For India—one of the world’s fastest-growing demand centers—the current global landscape presents both opportunities and challenges:

- Crude procurement costs may remain under pressure, supporting favourable import economics.

- Refining margins in Asia are expected to stay strong, influencing product price differentials and export economics.

- Rising global inventories may exert downward pressure on benchmark prices, which could translate into softer feedstock costs for domestic refiners.

- For downstream consumers and traders, the evolving supply-demand imbalance underscores the need for agile inventory and procurement strategies.

Conclusion

The Oil Market Report – November 2025 indicates that while global demand is recovering, supply growth continues to outpace consumption. Rising inventories, softening crude benchmarks, and strong refining margins collectively define the current market narrative. As the world approaches winter, the market will closely watch supply reliability, sanction impacts, and economic momentum across major economies.

Petrobazaar.com will continue to track these developments to support industry stakeholders with timely analysis, pricing insights, and data-driven perspectives.